Where Does Nj Property Tax Money Go

State and Local Backgrounders Homepage

A property taxation is a tax levied on "real property" (land and buildings, both residential and commercial) or personal property (concern equipment, inventories, and noncommercial motor vehicles).

Taxpayers in all 50 states and the District of Columbia pay property taxes, merely the taxation on real belongings is primarily levied by local governments (cities, counties, and school districts) rather than country governments. With a few exceptions, state property taxes are typically levied on personal holding.

- How much revenue practise state and local governments enhance from property taxes?

- Which states are most reliant on property tax revenue?

- How much do belongings taxation rates differ across the state?

- Farther reading

- Note

How much revenue practice state and local governments raise from property taxes?

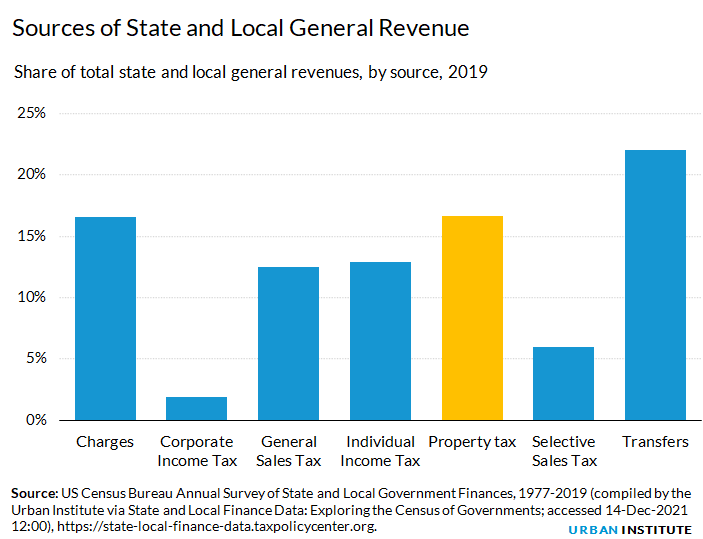

State and local governments collected a combined $577 billion in revenue from belongings taxes, or 17 percent of full general revenue, in 2019. Property tax revenue as a percent of country and local general revenue was higher than full general sales taxation revenue, individual income tax revenue, and corporate income revenue enhancement revenue in 2019.

Belongings taxes are a very small source of revenue for states considering states typically tax personal belongings but not real belongings. (Census does not provide a separate count for each type of belongings tax.) Country governments collected $18 billion from holding taxes in 2019, or i percentage of state full general acquirement. In contrast, property taxes are one of the largest sources of revenue for local governments. Local governments collected $559 billion in property taxes in 2019, or thirty per centum of local general revenue.

School districts, counties, municipalities, and townships all collect property tax revenue, and it typically accounts for a significant portion of general revenues in those jurisdictions—particularly for school districts. The remaining local government belongings tax revenue is collected by special districts that are specific-purpose units such every bit water and sewer government that typically get well-nigh of their revenue from taxes related to those services. (Census only publishes revenue totals for these levels of authorities for years ending in 2 and 7.)

| Local Belongings Revenue enhancement Revenue, by Level of Government, 2017 | ||

| Revenue ($ billions) | Percentage of general revenue | |

| School district | $212 | 37% |

| Canton | $120 | 28% |

| Municipality | $121 | 24% |

| Township | $34 | 62% |

| Special District | $22 | xi% |

| Note: The U.s. Census Bureau just publishes local-level data for years ending in 2 and 7. | ||

Which states are most reliant on property tax revenue?

All states have property taxes (at to the lowest degree at the local level). New Hampshire was the well-nigh reliant on belongings taxation acquirement in 2019, as the tax deemed for 36 percentage of its combined state and local general revenues. (New Hampshire does not have a broad-based individual income revenue enhancement or general sales taxation). The next near reliant states were New Jersey (29 percent), Maine (27 percent), and Connecticut (26 pct). Overall, ten states nerveless xx per centum or more of their state and local general revenues from belongings taxes in 2019.

Data: View and download each state'south general revenue by source as a percentage of general revenue

In dissimilarity, Alabama, Arkansas, Delaware, Kentucky, Louisiana, New Mexico, Oklahoma, and Westward Virginia nerveless less than 10 percentage of their state and local general revenue from property taxes.

Property taxes accounted for well-nigh half (46 per centum) of own-source local full general revenue (i.east., excluding transfers from the federal and country government). In Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, and Rhode Island, property tax collections were more than iii-quarters of local own-source general revenue in 2019. In contrast, Alabama's local governments collected just 21 pct of their ain-source acquirement from belongings taxes, the lowest percentage in whatever state.

At the country level, property taxes deemed for 1 percentage of country ain-source general revenue in 2019. However, Vermont's property taxes contributed 25 percent of its country own-source general revenue that year, far and abroad the highest percentage in any country. Well-nigh all of Vermont'southward instruction spending is financed at the country level, and the state'south property tax on real property is the largest source of that funding. The next-highest percentages were in New Hampshire and Washington (ix pct in both states), in part because these states also use property taxes to fund their land-level G-12 education spending.

Property taxes were also 7 percent or more of state own-source revenue in Arkansas, Montana, and Wyoming. In improver to business organization equipment and cars, state personal property taxes are sometimes levied on land that is used for utilities. Fourteen states did not levy a state-level property revenue enhancement in 2019.

The percentage of land and local full general acquirement from belongings taxes in a state reflects several factors, including:

- the property tax rates in a state'south local jurisdictions

- the value of the property in the state

- the relative amount of tax revenue in the state from other sources

How much do real property taxation rates differ across the land?

Real property taxation rates differ widely both across and within states, making it difficult to compare states against each other. Further, local governments use different methods to calculate their real property tax bases and assessment levels.

Every jurisdiction's property taxation requires at least three steps:

- Assess the value of each property in the jurisdiction.

- Determine the taxable value of each property.

- Utilize the tax charge per unit to the taxable value of each property.

The authorities levying the property tax typically assesses the real property value by estimating what the property would sell for in an artillery-length transaction (that is, a transaction between unrelated parties). Nonetheless, in that location are other calculations for assessing a holding's value. Some jurisdictions base their assessed value on the last sale toll or acquisition value of the property, the income a property could generate (e.thou., hotels), or solely on the size or physical attributes (e.grand., design or location) of the property. The timing of assessments also varies, with some jurisdictions assessing annually and others going multiple years between assessments.

Further, some jurisdictions impose their taxation on the entire assessed value of the belongings while others taxation merely a fraction of the assessed value. For example, South Carolina counties impose taxation on merely 4 percent of an possessor-occupied property's assessed value, while the Commune of Columbia taxes 100 percent of a holding'due south assessed value. Thus, the revenue enhancement rate in S Carolina counties is higher than the tax rate in the District of Columbia but that is not an apples-to-apples comparing.

Some local jurisdictions too impose dissimilar tax rates—or classifications—for unlike types of property, near commonly distinguishing between residential and business concern belongings.

And while property tax rates can vary considerably within states, some states impose a statewide limit on the maximum rate.

States and local governments likewise often use other limits, exemptions, deductions, and credits to lower a real holding'south taxable value or the taxpayer's payment for some or all owners. A few major examples are every bit follows:

- Assessment limits prevent a property'south assessed value from increasing by more than a fixed percent betwixt assessments. These limits generally reduce a property'due south assessed value below its actual market value and thus forestall rapid property value increases from raising the possessor's tax burden. When the belongings is sold, its assessed value is reset at its market value. Seventeen states and the District of Columbia offered some type of limitation on a property's assessed value in 2020. The holding eligible for an assessment limitation and the calculation of the limit (i.e., the percentage increase in assessment allowed over a time catamenia) varies across states.

- Homestead deductions or exemptions decrease the taxable value of real property by a fixed amount (much the same way a standard deduction decreases taxable income). While every state has residency requirements for claiming a homestead exemption, some states accept farther eligibility qualifications based on age, disability, income, or veteran status. Nearly every state and the District of Columbia broadly offered some type of homestead exemption or credit in 2018.

- Circuit breaker programs provide relief for elderly and low-income residents with property tax liabilities higher up a specified pct of their income. Although the taxation relief is based on property tax payments, information technology is typically provided via an private income revenue enhancement credit. Unlike the other approaches described here, circuit breakers can do good renters equally well as homeowners in some jurisdictions. Thirty-three states and the District of Columbia offered some form of circuit billow program in 2020. In 18 of these states and the District of Columbia, renters were eligible for the excursion breaker programme.

- Belongings tax deferrals allow elderly and disabled homeowners to defer payment until the auction of the holding or the death of the taxpayer. Twenty-iii states and the District of Columbia allowed such deferrals in 2020, just they are non widely used.

These relief programs can create significantly different tax burdens inside a jurisdiction even amid taxpayers who take homes of like vintage and pay the aforementioned tax charge per unit.

Further, while these policies can assist individual homeowners reduce their holding tax payments, diverse studies have shown that property taxation assessments and appeals outcomes can disproportionately help white homeowners and disproportionally burden Black and Latino households. This can make a locality'due south property taxation system more than regressive than it appears.

More detailed information on property tax relief and incentive programs, for all 50 states, can be found at the Lincoln Constitute'southward Property Tax Database.

Interactive data tools

Country and Local Finance Data: Exploring the Census of Governments

Land Fiscal Briefs

Farther reading

Pregnant Features of the Belongings Tax

Lincoln Constitute of Land Policy (2018)

Critics Contend The Property Tax Is Unfair. Do They Have A Point?

Tracy Gordon (2020)

The Cess Gap: Racial Inequalities in Property Taxation

Carlos Avenancio-León and Troup Howard (2020)

Source: https://www.urban.org/policy-centers/cross-center-initiatives/state-and-local-finance-initiative/projects/state-and-local-backgrounders/property-taxes

Posted by: vanhoutenmiteraid.blogspot.com

0 Response to "Where Does Nj Property Tax Money Go"

Post a Comment